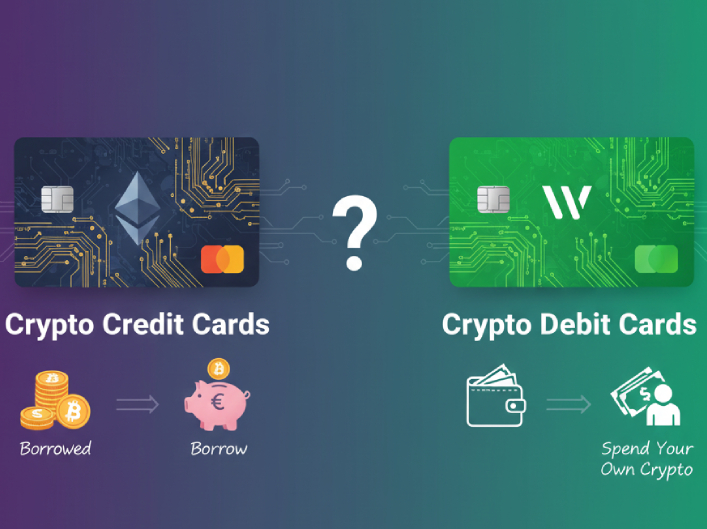

Many fintech users often confuse crypto debit cards with crypto credit cards, even though their financial structures work very differently. With a crypto debit card, you spend from your existing crypto balance, whereas with a crypto credit card, your cryptocurrency acts as collateral, allowing you to access a line of credit. In the following sections, we’ll break down the key differences in fees, settlement methods, and the benefits of each card.

What is a Crypto Card?

Modern financial technology has bridged the gap between digital assets and daily spending, making it easier than ever to use your Bitcoin or Ethereum at local merchants. If you are new to this ecosystem, you might find yourself asking, what is a crypto card? Simply put, it is a payment card that allows you to spend your cryptocurrency in the real world just like a traditional bank card, either by converting your coins to fiat instantly at the point of sale or by using a pre-funded balance. Understanding how these cards work is the first step toward achieving true financial flexibility in the Web3 era.

What is a Crypto Debit Card?

A crypto debit card is a financial bridge that allows you to spend your digital assets such as Bitcoin, Ethereum, or Stable coins at any merchant that accepts traditional payment networks like Visa or Mastercard. It functions exactly like a standard bank debit card, but instead of being linked to a fiat bank account, it is powered by your crypto wallet.

How It Works:

The magic happens at the point of sale. When you swipe your card or pay online, the card provider instantly converts the necessary amount of cryptocurrency into local currency (USD, EUR, etc.) to settle the transaction. This eliminates the need to manually sell your crypto on an exchange and wait days for a bank transfer.

Key Advantages:

- Instant Liquidity: You can turn your crypto into real world goods and services in seconds.

- Global Acceptance: Whether you are traveling, shopping online, or paying for subscriptions, these cards work at millions of locations worldwide.

- No Debt or Interest: Since it is a debit card, you are spending your own balance. You don’t have to worry about monthly interest rates or credit scores.

- Physical & Virtual Options: Most providers offer a virtual card for instant online use and a physical card for ATM withdrawals and in store shopping.

Important Considerations

While crypto debit cards offer incredible convenience, users should keep an eye on conversion rates and transaction limits. Additionally, remember that spending crypto is a “taxable event” in many jurisdictions, and once you spend your assets, you no longer benefit from any future price increases (bull runs) of those specific coins.

What is a Crypto Credit Card?

A crypto credit card allows you to access a line of credit using your digital assets as collateral. Unlike a debit card where you spend your own balance, a credit card lets you borrow funds from the provider to make purchases, while your cryptocurrency remains locked in a secure account.

How It Works:

When you use a crypto credit card, you aren’t selling your coins. Instead, you pledge your crypto (like Bitcoin or Ethereum) as collateral. The issuer gives you a credit limit based on the value of your assets. At the end of the month, you receive a bill. If you pay it back on time, your crypto stays untouched. If you fail to pay, the provider may liquidate your collateral to cover the debt.

Key Advantages:

- HODL While Spending: The biggest benefit is that you don’t have to sell your crypto. If the price of your Bitcoin doubles while it’s acting as collateral, you still gain from that increase.

- Build Credit Score: Some providers report your payment history to credit bureaus, helping you build a traditional credit profile.

- Liquidity Without Tax: In many countries, selling crypto triggers capital gains tax. By borrowing against it instead of selling, you can access cash without a taxable event.

- Higher Rewards: Credit cards often offer more premium rewards, such as higher cashback percentages or travel insurance.

The main risk is volatility. If the market crashes and the value of your collateral drops significantly, you might face a “Margin Call,” requiring you to add more crypto or risk having your assets sold by the provider. Also, keep an eye on the APR (Interest Rate) if you don’t plan to pay the full balance every month.

Which One Should You Choose? Crypto Debit vs. Credit Card

Choosing between a crypto debit and a credit card depends entirely on your financial goals and how you manage your digital assets. Both offer great flexibility, but they serve different purposes.

Choose a Crypto Debit Card if:

- You want to control your budget: Since you are spending your own pre-funded balance, there is no risk of overspending or falling into debt.

- You need it for daily expenses: It is the perfect tool for buying coffee, groceries, or paying monthly subscriptions without any interest fees.

- You prefer simplicity: There are no credit checks or monthly bills to worry about. You just load, spend, and repeat.

- You want to avoid market anxiety: By using stable coins (like USDT) on your debit card, you can enjoy stable purchasing power regardless of market volatility.

Choose a Crypto Credit Card if:

- You are a long term HODLer: If you believe your Bitcoin or Ethereum will be worth much more in the future, you shouldn’t sell it. Use a credit card to access cash while keeping your coins.

- You want to optimize taxes: Borrowing against your crypto is often not a taxable event, whereas selling it for a debit card purchase might be.

- You seek premium rewards: Credit cards typically offer higher cashback rates, airport lounge access, and travel perks.

- You want to build a credit history: If the provider reports to credit bureaus, it’s a great way to improve your financial standing in the traditional banking world.

Repayment: How it works with Topex

Managing your balance with Topex is designed to be as seamless as your spending. While traditional credit cards often impose a strict 30-day “grace period” before applying high-interest charges, a crypto backed system offers a more flexible approach to debt management.

Leverage Your Assets Without Selling

With a Topex debit card, your digital assets serve as your guarantee. This means you don’t have to liquidate your portfolio to access cash. You can maintain your position in the market while using a flexible line of credit for your global travels or business needs.

Zero Fee Repayment (The Top-up Advantage)

One of the standout features confirmed in the Topex ecosystem is the Free Top-up. When it’s time to settle your outstanding balance, you can add funds to your account without paying any extra loading fees. This ensures that every dollar you deposit goes directly toward clearing your debt, not into hidden service costs.

Flexible Settlement with Global Standards

Since Topex cards are fully integrated with Google Pay and Apple Pay, and operate on international networks (Visa/Mastercard), you have the convenience of managing your repayments through the Topex app. Whether you are using the Cashback, Travel, or Corporate card, the system is built to handle cross-border payments efficiently, allowing you to settle your balance in the currency that suits your plan.

Monitoring Your LTV

Because this is a collateral-based system, your main responsibility is monitoring your Loan-to-Value (LTV) ratio. As long as your crypto collateral maintains its value, you have significant flexibility in your repayment schedule. However, if the market shifts, Topex ensures the system’s stability by using the collateral to cover the balance, protecting both the provider and your remaining assets.

Conclusion

The choice between a crypto debit and credit card depends on your financial strategy: choose debit for simple, debt-free daily spending, or credit to access liquidity while keeping your assets for long-term growth. By leveraging Topex’s features, such as free top-ups and global payment integration, you can transform your cryptocurrency from a static investment into a versatile real-world tool. Whether you prioritize budget control or asset preservation, the right card ensures your digital wealth works effectively for your lifestyle.

FAQ

What is the main difference between a Crypto Debit and Credit Card?

With a Debit Card, you spend your own pre funded crypto balance. With a Credit Card, you borrow funds against your crypto (used as collateral) without selling your assets.

Do I need a credit check to get a Topex card?

No. Since these cards are backed by your cryptocurrency collateral, traditional credit scores are usually not required, making them accessible to a wider range of users.

Does using a crypto card trigger taxes?

In many jurisdictions, selling crypto or using a debit card is a taxable event. However, borrowing against your crypto (credit) is often not considered a sale and may help in tax optimization. Always consult with a tax professional.

What happens if the value of my collateral drops?

If the market price of your crypto decreases significantly, your LTV ratio will rise. You may need to add more collateral or pay back some of the loan to avoid a partial liquidation of your assets.