A crypto card is a payment card, physical or virtual, that lets you spend cryptocurrencies like Bitcoin, Ethereum, or USDT for everyday purchases, just as you would with a regular Visa or Mastercard. It works by either deducting funds from your crypto wallet and converting them to fiat at the point of sale (debit model) or by allowing you to spend on credit and earn crypto rewards (credit model). In this guide, we’ll break down how crypto cards work, the differences between types, fees, eligibility, real-world use cases, and how to choose the right one for your lifestyle.

So how exactly does a piece of plastic, or a virtual card sitting in your Apple Wallet, turn your Bitcoin into a cup of coffee in Berlin or a hotel room in Dubai? Let’s get into it.

Key Takeaways:

- A crypto card converts your digital assets into spendable fiat currency at the moment of purchase, making cryptocurrencies usable anywhere Visa or Mastercard is accepted.

- Crypto debit cards require pre-funding from your wallet, while crypto credit cards let you spend on credit and earn crypto rewards on each transaction.

- Most crypto cards require KYC verification, a minimum age of 18, and residency in a supported country before issuance.

- Typical fees include card issuance, top-up, ATM withdrawal, and conversion fees — though some providers like Topex charge only $1 for issuance and zero fees for top-ups.

- Crypto cards integrate with Apple Pay and Google Pay, enabling contactless and online payments globally without manual crypto-to-fiat conversion.

- Security features like two-factor authentication, advanced encryption, and instant card freezing make crypto cards safer than holding cash or transferring crypto manually.

- Stablecoins like USDT and USDC are widely preferred for daily card spending because they avoid volatility risk.

Crypto Card Meaning

A crypto card is a payment instrument that connects your cryptocurrency holdings to global payment networks, Visa, Mastercard, or local equivalents, so you can spend digital assets like fiat currency. The crypto card, in simple terms, is “a bridge between your crypto wallet and the real-world economy.”

Unlike a traditional bank card that draws from a fiat checking account, a crypto card draws from a wallet or exchange balance containing Bitcoin (BTC), Ethereum (ETH), stablecoins (USDT, USDC), or other supported assets. When you tap your card at a store, the issuer instantly converts the required amount of crypto into the merchant’s local currency. The merchant sees a standard card transaction; they don’t need to accept crypto themselves.

This is why crypto cards have become one of the fastest-growing tools in the Web3 economy: they remove the biggest friction point in crypto adoption, which is the lack of merchant acceptance.

Why Crypto Cards Matter Today

Crypto adoption has grown to hundreds of millions of users globally, yet direct merchant acceptance of crypto remains a small fraction of overall commerce. Crypto cards close that gap by leveraging existing card infrastructure. Crypto-linked card transactions continue to grow rapidly, signaling that users want to spend, not just hold, their digital assets.

How Do Crypto Cards Work?

Crypto cards work by linking your digital wallet or exchange account to a payment network, then automatically converting your selected cryptocurrency into fiat currency at the exact moment of a transaction. The process happens in milliseconds and is invisible to the merchant.

Here’s the typical transaction flow:

- You initiate a payment at a POS terminal, online checkout, or ATM.

- The card issuer checks your crypto balance in the connected wallet.

- The required crypto amount is converted to fiat at the current market rate.

- The fiat amount is sent to the merchant through the Visa or Mastercard network.

- The transaction settles, and your crypto balance is updated.

For credit-based crypto cards, the flow differs: the issuer pays the merchant in fiat instantly, and you settle the bill later, often with crypto rewards added to your account based on spending volume.

Behind the Scenes: The Conversion Engine

The real engineering happens in the conversion layer. Card issuers partner with liquidity providers and exchanges to lock in real-time exchange rates. Some providers convert crypto to fiat at the moment of authorization, while others maintain a pre-converted fiat balance on the card itself for faster settlement.

This is also why understanding the mechanics of going from crypto to fiat is critical; the conversion rate, slippage, and timing all affect how much purchasing power you actually get.

What Is a Crypto Credit Card?

A crypto credit card is a payment card that functions like a traditional credit card but rewards you with cryptocurrency instead of cashback, miles, or points. You spend in fiat on credit, pay off your balance later, and accumulate crypto rewards (typically 1–8% per transaction) that get deposited into your linked crypto account.

The main appeal is exposure to crypto markets without buying crypto directly. Every coffee, grocery run, or subscription payment slowly builds a crypto portfolio in the background.

How Crypto Credit Cards Differ From Crypto Debit Cards

This is one of the most common points of confusion for new users. The difference between crypto debit cards and crypto credit cards comes down to funding source, credit risk, and reward structure.

| Feature | Crypto Debit Card | Crypto Credit Card |

|---|---|---|

| Funding | Pre-loaded from crypto wallet | Spend now, pay later |

| Credit Check | Usually not required | Required |

| Rewards | Sometimes, varies by issuer | Crypto rewards on every purchase |

| Risk | Limited to loaded balance | Debt risk if unpaid |

| Availability | Global, fewer restrictions | Mostly U.S. and select markets |

| Best For | Daily spending, travel, budgeting | Building crypto holdings via spending |

In short, a crypto debit card spends your crypto, while a crypto credit card spends the issuer’s money and pays you in crypto.

Types of Crypto Cards

Crypto cards fall into several categories beyond the basic credit vs. debit distinction. Knowing which type fits your needs avoids unnecessary fees and limitations.

- Custodial Crypto Cards: The exchange or issuer holds your crypto. Easier to use but requires trust in the provider.

- Non-Custodial Crypto Cards: You keep control of your private keys via a self-custody wallet. More secure but technically demanding.

- Prepaid Crypto Cards: Loaded with a fixed amount, no overdraft. Good for budgeting and gifting.

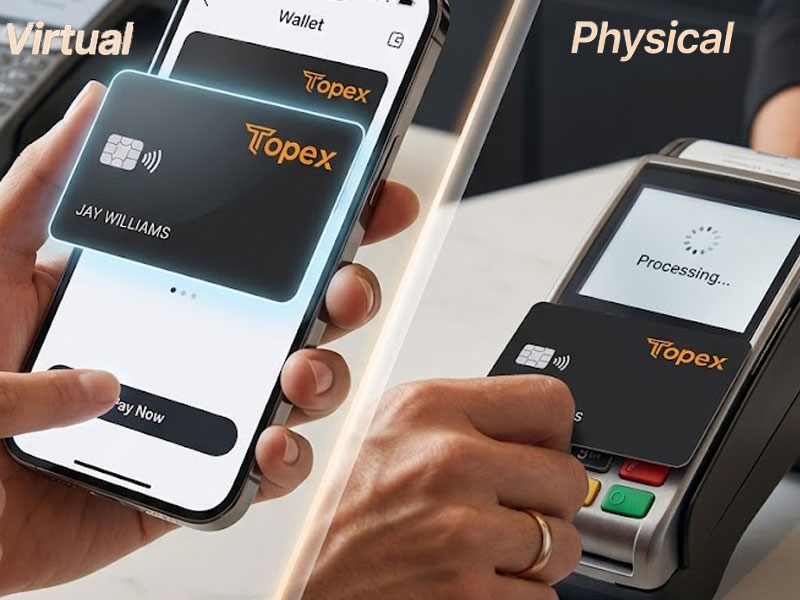

- Virtual Crypto Cards: Digital-only, generated instantly for online use. Often used with Apple Pay or Google Pay.

- Physical Crypto Cards: Plastic or metal cards for in-person use and ATM withdrawals.

- Corporate Crypto Cards: Designed for businesses to manage expenses, payroll, and international transactions.

Virtual vs. Physical: Which One Should You Get?

For users who shop primarily online or travel light, a virtual card is faster to issue and harder to steal physically. For travelers, freelancers, or anyone needing ATM access, a physical card remains essential. Many providers issue both, so you don’t have to choose.

How to Get a Crypto Card

Getting a crypto card is straightforward and usually takes less than 15 minutes if you have your documents ready. Here’s the standard process:

- Choose a provider that supports your country, your preferred cryptocurrencies, and your spending habits.

- Sign up and complete KYC verification by submitting a government-issued ID and a selfie. Some providers also require proof of address.

- Fund your account by transferring crypto from an external wallet or buying directly on the platform.

- Apply for the card, choose between virtual, physical, or both.

- Wait for approval and delivery. Virtual cards activate within minutes; physical cards typically arrive in 7–21 days.

- Activate the card and link it to Apple Pay or Google Pay for instant mobile use.

If you’re wondering exactly what the requirements are for crypto cards in your specific region, including age limits, document types, and supported nationalities, the requirements vary slightly between providers, so check before applying.

How to Use a Crypto Card

Once activated, using a crypto card is identical to using a regular Visa or Mastercard. Tap, swipe, insert, or pay online; the card handles the crypto-to-fiat conversion automatically.

Here are the main ways to use a crypto card:

- In-store payments via contactless tap or chip-and-PIN.

- Online shopping involves entering card details at checkout.

- Mobile wallets like Apple Pay and Google Pay for tokenized, secure payments.

- ATM withdrawals to get local cash anywhere in the world.

- Recurring subscriptions like Netflix, Spotify, or SaaS tools.

- Travel bookings including flights, hotels, and car rentals.

Best Practices for Daily Use:

A few habits will save you money and headaches:

- Keep a stablecoin balance (USDT or USDC) for daily spending to avoid volatility.

- Hold volatile assets like BTC or ETH as a long-term position, not your spending balance.

- Enable transaction notifications and 2FA from day one.

- Use the card’s freeze function whenever you’re not actively spending.

How to Top Up a Crypto Card

Topping up a crypto card means moving crypto from your wallet into your card’s spending balance. The process is fast and usually free with modern providers.

The standard steps for how to top up a crypto card are:

- Log in to the issuer’s app or web dashboard.

- Open the “Card” or “Wallet” section.

- Select “Top Up” or “Load Funds.”

- Choose the cryptocurrency (BTC, ETH, USDT, etc.) and amount.

- Confirm the transaction.

- Wait for blockchain confirmations, usually under a few minutes.

Once confirmed, your card balance updates automatically, and you’re ready to spend.

Common Top-Up Mistakes to Avoid:

- Sending crypto to the wrong network (e.g., USDT on TRC-20 when only ERC-20 is supported).

- Topping up volatile assets right before a market drop.

- Ignoring minimum top-up thresholds can cause transactions to fail.

What You Should Know About Crypto Card Fees

Fees are where crypto cards differ the most. Some providers nickel-and-dime users with hidden charges, while others operate with full fee transparency.

Here are the most common fees you’ll usually come across:

- Card Issuance Fee: One-time charge for ordering the card.

- Top-Up Fee: Charge for loading crypto onto the card.

- Conversion Fee: Spread between crypto and fiat at the moment of purchase.

- Monthly/Annual Maintenance Fee: Subscription cost for keeping the card active.

- ATM Withdrawal Fee: Charged per cash withdrawal, plus possible foreign ATM fees.

- Foreign Transaction Fee: Applied when spending in a non-base currency.

- Inactivity Fee: Charged if the card isn’t used for a set period.

Before choosing a card, request a full fee schedule. The lowest headline fee isn’t always the cheapest in real-world use.

Supported Cryptocurrencies and Networks

Most crypto cards support a core set of cryptocurrencies, but the exact list varies. The most commonly supported assets are:

- Bitcoin (BTC): The default option on nearly every crypto card.

- Ethereum (ETH): Universally supported.

- Stablecoins (USDT, USDC, DAI): Increasingly preferred for daily spending due to price stability.

- Major Altcoins: Solana (SOL), Cardano (ADA), XRP, BNB, depending on the provider.

Why Stablecoins Are Becoming the Default

Stablecoin-based card spending has become a major share of all crypto card transactions. The reason is simple: nobody wants to spend $50 worth of Bitcoin on lunch only to watch BTC pump 10% the next day. Stablecoins eliminate that regret.

Differences Between Crypto Cards and Traditional Debit or Credit Cards

Traditional cards draw from a bank account in fiat. Crypto cards draw from a digital wallet and convert crypto in real time. That single difference unlocks several practical advantages.

| Feature | Traditional Card | Crypto Card |

|---|---|---|

| Funding Source | Bank account (fiat) | Crypto wallet or exchange |

| Banking Required | Yes | No |

| Setup Time | Days to weeks | Minutes to hours |

| Global Access | Subject to bank restrictions | Borderless |

| Asset Type | Fiat only | Crypto + fiat conversion |

| Best Use Case | Domestic spending, payroll | Global, online, crypto-native lifestyle |

Crypto cards also remove the dependency on traditional banking, a major benefit for freelancers, digital nomads, and users in regions with limited banking infrastructure.

Benefits of Using a Crypto Card

A well-chosen crypto card delivers real, measurable value. Here are the most impactful crypto card benefits:

- Instant Spending of Digital Assets: No need to sell crypto on an exchange and wait for bank transfers.

- No Bank Account Required: Get a functional payment card without opening a checking account.

- Global Acceptance: Use the card at millions of Visa/Mastercard merchants worldwide.

- Mobile Wallet Integration: Tap-to-pay through Apple Pay and Google Pay.

- Advanced Security: Encryption, 2FA, instant freeze, and tokenized payments.

- Borderless Payments: Spend the same balance in any country without currency exchange visits.

- Privacy-Friendly Options: Some providers minimize personal data exposure compared to banks.

- Faster Onboarding: KYC and approval in minutes instead of days.

For a deeper look into whether the convenience and savings outweigh the fees and risks for your specific situation, see our analysis on whether a crypto card is worth it.

Security: How Safe Are Crypto Cards?

Modern crypto cards are generally as secure as, and often more secure than, traditional cards. The combination of advanced encryption, two-factor authentication, biometric verification, and instant in-app controls gives users real-time protection.

Reputable providers implement several layers of defense:

- PCI-DSS Compliance: The same security standard required of major banks.

- Tokenization: Card numbers are replaced with secure tokens during transactions.

- 2FA and Biometrics: Required for logins, transfers, and large purchases.

- Instant Freeze/Unfreeze: One-tap card control inside the app.

- Cold Wallet Storage: Reputable issuers keep the majority of user crypto in offline storage.

- 24/7 Fraud Monitoring: AI-driven transaction analysis to flag suspicious activity.

For users specifically focused on secure crypto payments, prioritize cards from providers with proven compliance records, transparent custody policies, and a strong fraud response track record.

Risks to Be Aware Of:

No system is risk-free. Be mindful of:

- Price Volatility: Spending BTC before a price spike means missed gains.

- Regulatory Changes: Some countries restrict or ban crypto cards entirely.

- Custodial Risk: If the issuer fails, custodial funds may be at risk.

- Phishing and Social Engineering: The weakest link is usually the user, not the technology.

Real-World Use Cases for Crypto Cards

Crypto cards aren’t just for crypto enthusiasts anymore. They’ve quietly become essential tools for several user groups.

- Freelancers and Remote Workers: Receive crypto payments globally and spend them locally without intermediary banks.

- Digital Nomads and Travelers: Avoid foreign transaction fees and currency exchange hassles.

- Online Shoppers: Pay for subscriptions, e-commerce, and digital goods directly from crypto.

- Crypto Investors: Spend small portions of holdings without triggering large taxable events.

- Underbanked Users: Access global payments without traditional banking infrastructure.

- Businesses: Manage corporate expenses, pay international suppliers, and reconcile transactions with on-chain transparency.

Travel: A Standout Use Case

Crypto cards genuinely shine when you’re abroad. No foreign transaction fees from your home bank, no need to carry multiple currencies, and instant conversion to local fiat at competitive rates. If you’re researching where to buy a crypto card for travel, prioritize providers with low FX spreads, broad ATM coverage, and built-in travel features.

Topex Crypto Card: A Practical Example of How Modern Crypto Cards Should Work

Topex represents the new generation of crypto cards built around transparency, speed, and global usability. Instead of burying fees and complicating onboarding, Topex offers a straightforward proposition: spend your crypto directly, anywhere, with no hidden costs.

Here’s what makes the Topex card stand out:

- Card issuance fee is only $1: One of the lowest entry points in the industry.

- Free top-ups: Loading crypto onto your card costs nothing.

- Full fee transparency: Zero hidden charges.

- Fast KYC: Simple identity verification with quick approval.

- Apple Pay and Google Pay support: Add the card to your mobile wallet for tap-to-pay.

- Accepted at millions of POS terminals and online gateways worldwide: Spend globally without restrictions.

- Advanced transaction encryption: High-grade security on every payment.

- 24/7 dedicated customer support: Help is available any time, any day.

With Topex, your digital assets are always ready to spend. You don’t need to navigate complex exchange processes or wait for crypto-to-fiat conversions; purchases happen directly and instantly. You can also use TopexCard with Apple and Google Pay to make contactless payments at any compatible terminal, turning your phone or smartwatch into a crypto-powered wallet.

“We believe in transparency. Topping up your card is completely free, and the card issuance fee is just $1. There are absolutely no hidden fees.”

Whether you’re traveling, shopping online, or managing daily expenses, Topex turns your crypto into borderless, frictionless spending power.

Eligibility and Requirements for Getting a Crypto Card

Eligibility varies by provider, but the core requirements are consistent across the industry. Most users will need to meet the following:

- Minimum age of 18 (some regions require 21).

- Legal residency in a supported country: Always check the provider’s coverage list.

- Government-issued ID: Passport, national ID, or driver’s license.

- Proof of Address: Utility bill or bank statement, dated within the last 3 months.

- Selfie or Liveness Check: For KYC and anti-fraud verification.

- Compliant Source of Funds: Some providers require proof of crypto origin for large balances.

Restricted Regions:

Crypto cards are typically unavailable in countries with strict crypto bans or sanctions. Always verify your jurisdiction before applying.

The Future of Crypto Cards

Crypto cards are evolving fast. The next wave of innovation will likely focus on deeper blockchain integration, lower fees, and broader merchant acceptance.

Expect to see:

- Direct stablecoin settlement: Merchants receive stablecoins instead of fiat, reducing conversion costs.

- On-chain rewards programs: Tokenized loyalty systems with real liquidity.

- DeFi integration: Cards linked to lending protocols, allowing users to spend against collateral.

- CBDC compatibility: Central bank digital currencies sharing infrastructure with crypto cards.

- AI-driven fraud detection: Real-time, predictive transaction security.

- Wider native crypto acceptance: Merchants are increasingly accepting crypto directly, with cards bridging the gap during transition.

As adoption grows, crypto cards are on track to become as common as contactless cards, a routine part of how people pay, not a niche tool.

Final Thoughts on What Crypto is

Crypto cards have moved from being a novelty for early adopters to becoming a genuine financial tool for anyone who holds digital assets. The right card removes the friction between crypto and daily life, letting you spend, travel, shop, and manage money without constantly converting between worlds.

The smartest approach is to choose a provider that prioritizes transparency, low fees, strong security, and global usability. A card with a high issuance fee and hidden FX spreads costs more than a card with honest pricing, no matter how flashy its rewards program looks on the surface. Focus on real-world usability, real fees, and real protection; that’s what separates a good crypto card from a great one.

If you hold crypto and want it to actually do something for you, a well-chosen crypto card is one of the most practical upgrades you can make to your financial setup.

Key Questions About What Crypto is

What is a crypto card, and how does it work?

A crypto card is a payment card that lets you spend cryptocurrency for everyday purchases. It works by converting your crypto into local fiat currency at the moment of purchase, so the merchant receives a normal card payment while you spend from your crypto wallet.

What’s the difference between a crypto debit card and a crypto credit card?

A crypto debit card spends crypto you already own by converting it to fiat instantly. A crypto credit card lets you spend on credit in fiat and earns crypto as a reward on each transaction, similar to a traditional rewards credit card.

Are crypto cards safe to use?

Yes. Reputable crypto cards use advanced encryption, two-factor authentication, tokenized payments, and instant freeze controls. As long as you choose a regulated provider with strong custody practices and follow basic security habits, crypto cards are as safe as, and often safer than, traditional bank cards.

Do I need a bank account to get a crypto card?

No. One of the main advantages of crypto cards is that they don’t require a traditional bank account. You only need a crypto wallet, identity verification, and residency in a supported country.

Which cryptocurrencies can I use with a crypto card?

Most crypto cards support Bitcoin (BTC), Ethereum (ETH), and major stablecoins like USDT and USDC. Some providers also support altcoins like Solana, Cardano, and XRP. Stablecoins are recommended for daily spending to avoid price volatility.